Business value determine share price or Share price determines the value

In school and college in economics & finance, we learned that asset prices move towards their fundamental value in long term but can a change in asset prices in financial markets cause a change in business value?

George Soros might have the answer

In his book “Alchemy of Finance” he disposes of the equilibrium theory according to which prices in the long run at equilibrium reflect the underlying economic fundamentals, which are unaffected by prices. Recognizing this has been sacrificed because the human mind wants certainty whereas uncertainty is a key feature of human affairs.

He says- “Financial markets can create inaccurate expectations and then change reality to accord with them. This is the opposite of the process described in textbooks and built into economic models, which always assume that financial expectations adapt to reality, not the other way round.”

Reflexivity proposes that financial market prices influence the fundamentals of a business and that these newly influenced sets of fundamentals then proceed to change market expectations, thus influencing prices; the process continues in a boom/ bust cycle. In situations with thinking participants, the participants’ view of the world is mostly half-baked & distorted. These distorted views can influence the situation to which they relate because false views lead to inappropriate actions.

Reflexivity refers to the virtuous effect of market sentiment, whereby rising prices attract buyers whose actions drive prices higher still until the process becomes unsustainable. This is an instance of a positive feedback loop. The same process can operate in reverse leading to a catastrophic collapse in prices.

In the real world, the investors’ thinking leads to various actions and not only wishful thinking. The investors’ views influence the course of events, and the course of events influences the investors’ views leading to a continuous feedback loop. Let us see some current examples of both positive and negative feedback loops.

Let’s take the example of the most talked-about fund in the world, ARKK.

ARKK’s shares peaked at $159 in mid-February and were down more than 35% some days ago. ARK Invest’s Cathie Wood has begun to engage in a potentially dangerous strategy – of raising liquidity by selling more liquid, large-cap tech stocks (e.g., Amazon (AMZN) and Facebook (FB) ) in favor of buying higher octane, more volatile small-cap tech stocks in which ARK has a substantially rising percentage of float/outstanding shares.

Should tech shares continue to decline and ARK Invest ETFs’ redemptions accelerate – the absence of liquidity will be profound and it is possible that a “flash crash” (and loss of liquidity ) in some of their ETFs. Since ARKK is holding significant stakes in these mid-cap tech & innovation stocks (more than 5% of free float), any serious redemptions might put a significant dent in the share prices. Since most of these businesses are in the investment phase of rapid growth, they would have to do higher dilution at depressed prices & due to negative perception & fear among market participants they might not be able to raise capital, leading to scaling down/ shutdown of businesses in future.

Let us take another example of the most talked about and feared crashes in history, the Global Financial Crisis of 2008 where the negative feedback loop played out.

The triggers for the GFC were falling US house prices and a rising number of borrowers’ inability to repay their loans. House prices in the United States peaked around mid-2006, coinciding with a rapidly rising supply of newly built houses in some areas. As house prices began to fall, the share of borrowers that failed to make their loan repayments began to rise. The credit ratings of borrowers fell and they were not able to refinance the mortgages leading to widespread defaults.

Let’s come closer back home and use these frameworks to see how the Franklin and NBFC crisis unfolded.

Around the time Covid stuck, the majority of Franklin India Credit Risk fund investments were in AA and below. This led to fear among investors of a potential default leading to widespread redemptions. Given the size of the AMC, Franklin was sometimes the sole lender to some corporates. Due to sudden redemption pressure at Franklin’s end, some leveraged companies were not able to repay the debt at such short notice and had to slow down their growth/ declare bankruptcy showing us again that in situations with thinking participants, distorted views can influence situations leading to change in equilibrium.

Now let us see the positive feedback loop in action by taking a few examples in India.

One of the fastest-growing consumer NBFCs in India, Bajaj Finance did a QIP of 8500 crores in late 2019 at INR 4000/ share leading to dilution of equity at ~8x P/B. Now imagine if the company wanted growth capital a few months down the line when the share price was below 2000/ share the dilution would have been larger and would likely be viewed negatively by investors. Due to the low dilution and high quality of its book, BAF has been able to grow in a calibrated manner and is capturing market share even in these unprecedented times.

The same was the case with Info edge doing an 1875 cr QIP and Indiamart doing a 1000 cr QIP at 8615/share in Feb 2021 when technology stocks were the flavor of the season making them build up a war chest for future growth and contingencies. This makes me remember a famous quote in investing circles “Raise money when you don’t need it for you might not get it when you desperately need it”.

Investment implications

We at Perennial, Ex financials generally participate in businesses that generate huge free cash flows and reinvest them for growth. Our portfolio level 3 year EBITDA growth is 20% with a net cash balance sheet and ROE of ~26%.

In lenders, we stick with the best of best and keep a tab on the price of the businesses as they may be a precursor to fundamental deterioration.

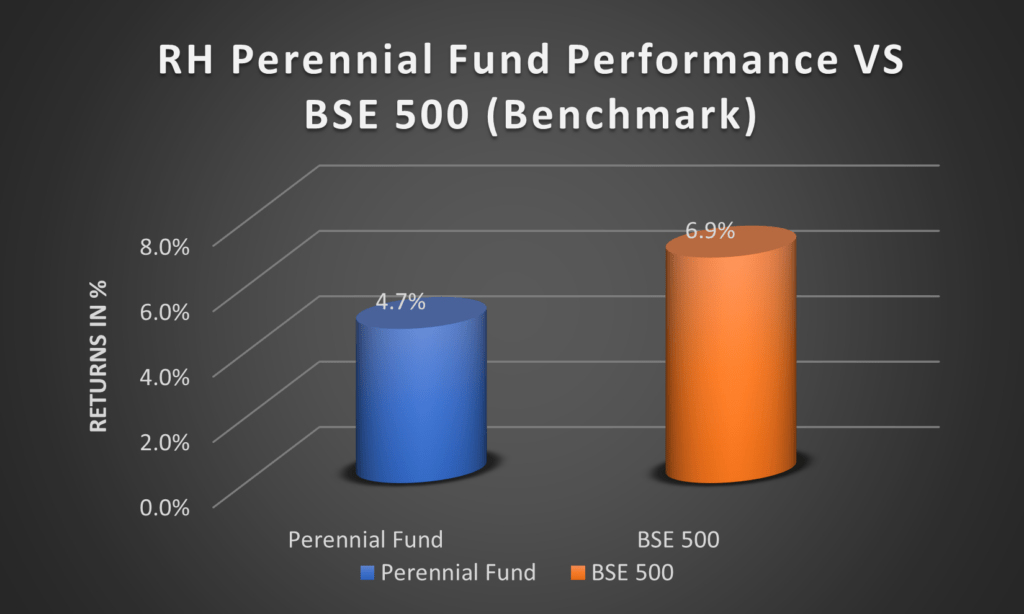

Performance update of the RH Perennial Fund

Our core focus is purely on wealth creation by focusing on identifying major wealth creation trends, monopolistic & fast-growing capital-efficient franchises with reinvestment runways run by able & minority friendly management sticking to our core philosophy of growth at a reasonable price. Our proprietary “fraud search” & “forensic accounting” framework helps us weed out poor quality businesses & promoters. While our qualitative judgment helps us identify the moats of perennial champions.

Returns are as of May 31, 2021

Returns are shown net of fees & transaction costs

RH Perennial Fund is regulated by the Securities and Exchange Board of India as a provider of Portfolio Management Services (SEBI Registration No. IINA200002601). The information provided in this newsletter does not, and is not intended to, constitute investment advice; instead, all information, content, and materials available in this newsletter are for general informational purposes only. It is safe to assume that we have allocations to all stocks mentioned here and may also sell them without prior notice. The information on this website may not constitute the most up-to-date information. The enclosed material is neither investment research nor a piece of investment advice. The contents and information in this document may include inaccuracies or typographical errors and all liability with respect to actions taken or not taken based on the contents of this newsletter are hereby expressly disclaimed. The content in this newsletter is provided “as is,” no representations are made that the content is error-free. No reader, user, or browser of this newsletter should act or refrain from acting on the basis of information in this newsletter without first seeking independent advice in that regard. Use of, and access to, this website or any of the links or resources contained within the site do not create a portfolio manager-client relationship between the reader, user, or browser and website authors, contributors, and their respective employers. The views expressed in, or through, this site are those of the individual authors writing in their individual capacities only.