We often get asked as to why do we have such a high allocation to the healthcare sector compared to other multi-cap funds. We start our argument with a quote from Pat Dorsey, one of the best minds in investing- “Most people could survive without gourmet coffee or the latest DVD player, but healthcare is one of the few areas of the economy directly linked to human survival & so important is animal’s survival” Essentially, we at Perennial are looking at sectors with consolidating profit pools, monopolistic & fast-growing capital-efficient franchises with reinvestment runways run by able & minority friendly management sticking to our core philosophy of growth at a reasonable price and the healthcare sector fit the bill perfectly.

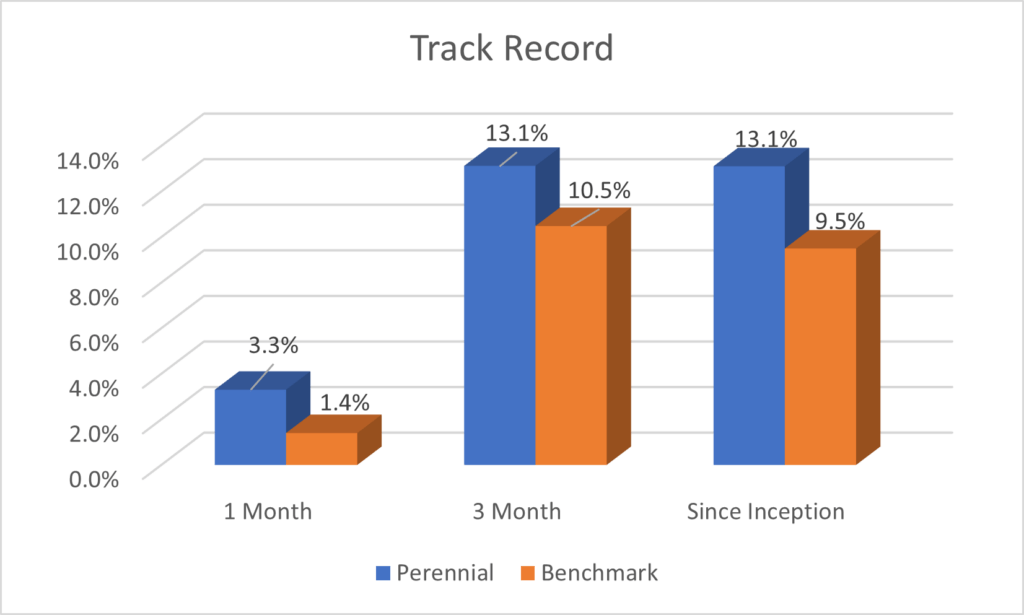

Performance update

We at Perennial look for anti-fragile business models, i.e companies that can compound our wealth irrespective of the economic conditions.

Fund Performance Vs Benchmark

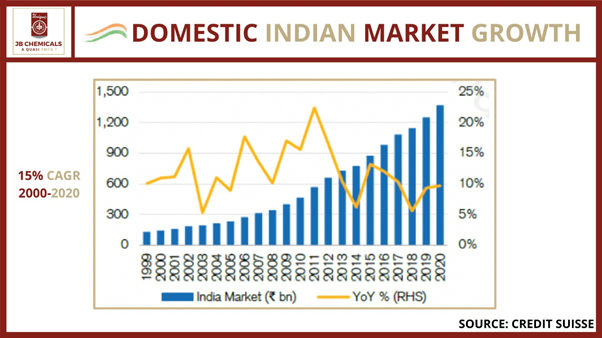

The Indian pharma industry is the epitome of that and has grown at 15% CAGR over the last 20 years.

The sector many businesses which fit into the “dull, drab & boring category” with very good unit economics & cash flows which are hitherto ignored by the analyst community at large.

Given this framework, we will take you through a few champion franchises we have identified for perennial wealth creation.

Syngene International- Value migration from Boston to Bangalore?

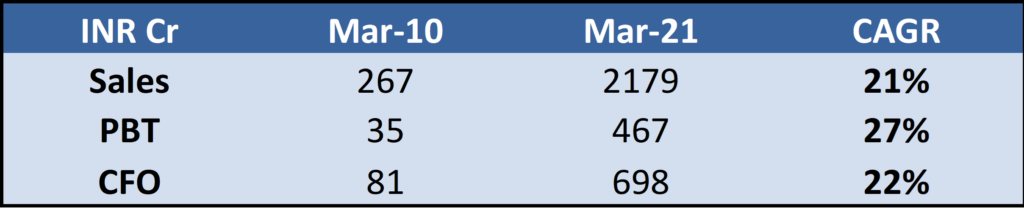

Syngene is a CRAMS player offering integrated drug research, development & manufacturing across life sciences & other sectors. It has scaled up its Sales, PBT, CFO upwards of 20% over the last decade.

Global innovation, Indian costs- Just like the Indian IT Sector was built upon the availability of high-quality employees at fraction of the costs of developed markets, the same trend can be seen in the CRAMS sector with high-quality English-speaking scientists in India. Syngene’s India billing rate per scientist is 60k USD v/s China’s 100k & Western Companies’ 175k. Also, in case the client doesn’t outsource then the internal cost per scientist for the client works out to be ~250k/ scientist.

Partner of choice for outsourcing- With increased outsourcing by innovator pharma companies, CRAMS space is expected to see hockey-stick growth. Syngene, one of the largest contract research employers globally has acquired critical mass in innovative discovery & will be a preferred partner due in wake of tight delivery schedules, end-to-end project management requirements & massive scale-up/ down requirements of innovator pharma.

One-stop platform- From discovery research to selecting a molecule to take it forward to human studies & commercial manufacturing, Syngene has developed best practices. We feel scale-up of the newly built Mangalore facility has the potential to take Syngene to newer orbits.

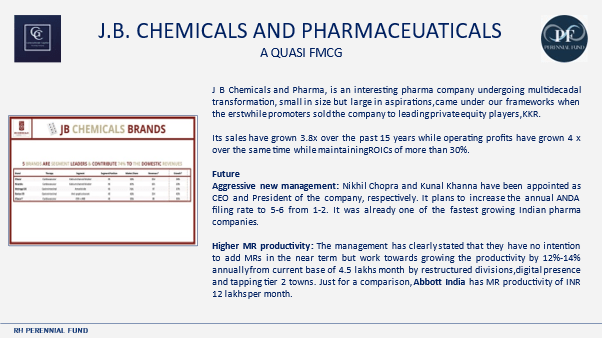

JB Chemicals & Pharma- a quasi FMCG?

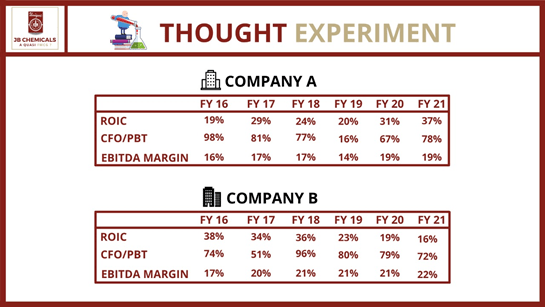

We conducted an interesting thought experiment in May https://perennialfund.in/jb-chemicals-a-quasi-fmcg/. Let us revisit that again to showcase market inefficiencies.

We leave it to you to guess which one is an FMCG company trading at 45 times earnings, and which one is a pharma company trading at 25 times earnings. We notice that both companies have sustainably high ROICs, great CFO/PBT conversions, and decent EBITDA margins, with company A faring relatively better. To clear the suspense, Company A is J B Chemicals whereas, Company B is Godrej Consumer Products.

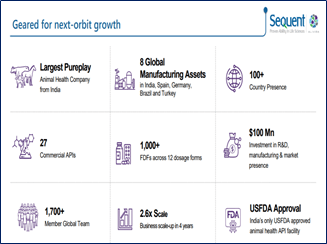

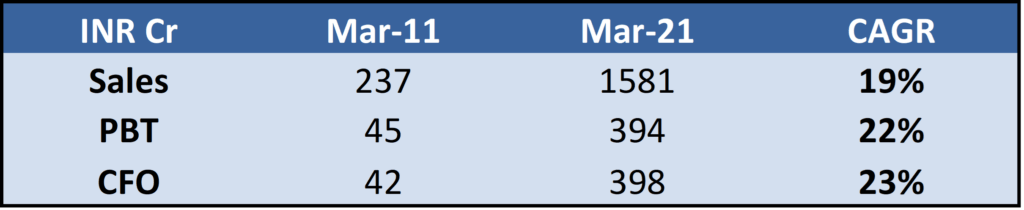

Sequent Scientific- An MNC pharma in making?

Sequent Scientific is the largest pure-play animal healthcare business in India which came under our radar after one of the leading global private equity firms, the Carlyle group took control of it. Why do we like the business?

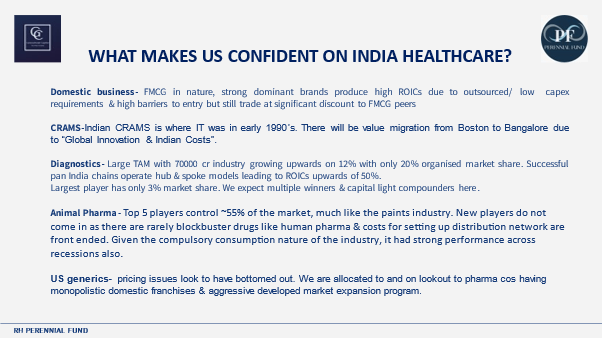

Excellent industry structure- Top 5 players control ~55% of the market, much like the paints industry. New players do not come in as there are rarely blockbuster drugs like human pharma & costs for setting up distribution networks are front-ended. Given the compulsory consumption nature of the industry, it had strong performance across recessions also.

- Large Opportunity Size: At Perennial, We like to invest in companies that have a large Total Addressable market Global animal health market size is projected to grow at a CAGR of 4.9% to reach US$46.1 billion by CY26. SeQuent, has strong capabilities to capitalize on these emerging opportunities. Sequent has emerged among the ‘Top 3’ USFDA Veterinary Master File (VMF) filers.

Many developed countries’ pharmaceutical companies rely on China for active pharmaceutical ingredients (APIs). In the given circumstances, this is expected to shift from China to other manufacturing bases including India and local manufacturing in Europe and USA.

- Optionality- Going ahead, we see Sequent for becoming a partner of choice for Top 5 players for India distribution along with potential entry into more high margin businesses.

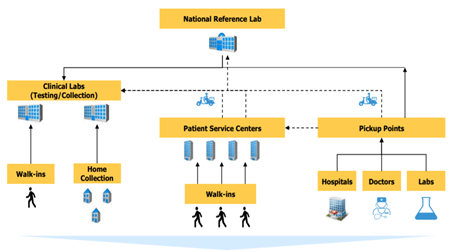

Dr. Lal Path Labs- Free Cash Flow machine

Dr. Lal Path Labs is a dominant consumer healthcare brand in the diagnostics sector having scaled up its Sales/ Profits/ Cash flow from operations over 20% over the last decade along with a long runway for growth and total addressable market.

Dominant Capital light compounder – franchise model saves investment in new stores and generates 25-30% commission on revenues earned by franchisees leading to ROCE of 86% (excl. cash) & cash on books touching 1000 cr.

- Scale begets scale- Being the largest pan Indian diagnostics chain in India, Dr. Lal is able to negotiate better reagent rentals along with pan India trust of doctors due to NABL accreditation leading to virtuous cycle of trust & profitability

- Unique hub & spoke model- Scalable model integrated through centralized IT platform allows network expansion.

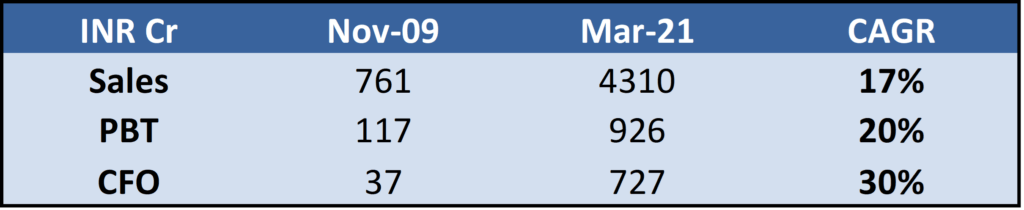

Abbott India- the ultimate capital-light compounded

Abbott India is one of the fastest-growing listed MNC pharma companies recording superlative ~11-year financial performance with industry-beating Sales, PBT & Cash flow from operations CAGR of 17%, 20% & 30% with ROICs averaging ~95% over the past ~11 years.

A quasi FMCG- The top 10 brands of Abbott India rank either as #1 or #2 in their respective application areas – for instance, Thyronorm (treating Thyroid), Digene( for treating antacid), Duphaston (infertility/miscarriages), Vertin (Vertigo). Due to the brand equity of its brands & parent company, it gets products made by the third party while owning sales & distribution with a focus on the chronic segment with longevity along with minimum R&D spend due to supply by the parent.

- Razor sharp focus- While most big pharma in India are focused on building generic outsourcing model which has low branding & pricing power, more cash burn & regulations, Abbott India focused on brand creation, product innovation & supply chain efficiencies leading to fixed asset turnover above ~10x & negative working capital cycle.

- We expect future launches of newproducts from its key divisions, along with brand extensions and access toinnovative molecules from global parent to drive growth.

RH Perennial Fund is regulated by the Securities and Exchange Board of India as a provider of Portfolio Management Services (SEBI Registration No. IINA200002601). The information provided in this newsletter does not, and is not intended to, constitute investment advice; instead, all information, content, and materials available in this newsletter are for general informational purposes only. It is safe to assume that we have allocations to all stocks mentioned here and may also sell them without prior notice. We have current allocations to J B Chemicals & Pharmaceuticals, Sequent Scientific, Abbott India, Dr Lal Path Labs & Syngene International. The information on this website may not constitute the most up-to-date information. The enclosed material is neither investment research nor a piece of investment advice. The contents and information in this document may include inaccuracies or typographical errors and all liability with respect to actions taken or not taken based on the contents of this newsletter are hereby expressly disclaimed. The content in this newsletter is provided “as is,” no representations are made that the content is error-free. No reader, user, or browser of this newsletter should act or refrain from acting on the basis of information in this newsletter without first seeking independent advice in that regard. Use of, and access to, this website or any of the links or resources contained within the site do not create a portfolio manager-client relationship between the reader, user, or browser and website authors, contributors, and their respective employers. The views expressed in, or through, this site are those of the individual authors writing in their individual capacities only.